How to Secure Your First Fix and Flip Loan as a Beginner

Fix and flip loans for beginners can feel overwhelming at first, but getting your first deal funded is more straightforward than most people think. But for most beginners, the financing part feels like a wall. What kind of loan do you need? What do lenders actually look for? How do you compare offers without getting burned?

This guide walks you through the entire process, step by step, so you can walk into your first deal prepared and confident.

What Is a Fix and Flip Loan?

A fix and flip loan is a short-term loan designed specifically for real estate investors who buy distressed properties, renovate them, and sell for a profit. Unlike a traditional mortgage, which is built for long-term homeownership, a fix and flip loan is structured around the deal itself.

Key characteristics:

- Term: Typically 6 to 18 months

- Purpose: Purchase plus renovation costs

- Repayment: Usually paid off when the property sells

- Approval basis: Based more on the property’s potential value than your personal credit score

The two most common types beginners encounter are hard money loans and bridge loans.

Hard money loans come from private lenders or lending companies rather than banks. They close fast (sometimes in 7 to 10 days), have higher interest rates (typically 8 to 15%), and are ideal when speed matters more than getting the lowest rate. Most experienced flippers use hard money loans because the ability to close quickly often wins deals that slower bank financing would lose.

Bridge loans are similar short-term loans that bridge the gap between buying a property and either selling it or securing permanent financing. They tend to have slightly lower rates than hard money but may take longer to close.

For most first-time flippers, a hard money loan through a private lender is the fastest and most accessible path to getting your first deal funded.

Step 1: What Lenders Look For When Reviewing Fix and Flip Loans for Beginners

Before you apply for anything, it helps to understand how lenders think. Hard money lenders are primarily asset-based, meaning they care more about the property and the deal than your personal financial history.

Here is what most lenders evaluate:

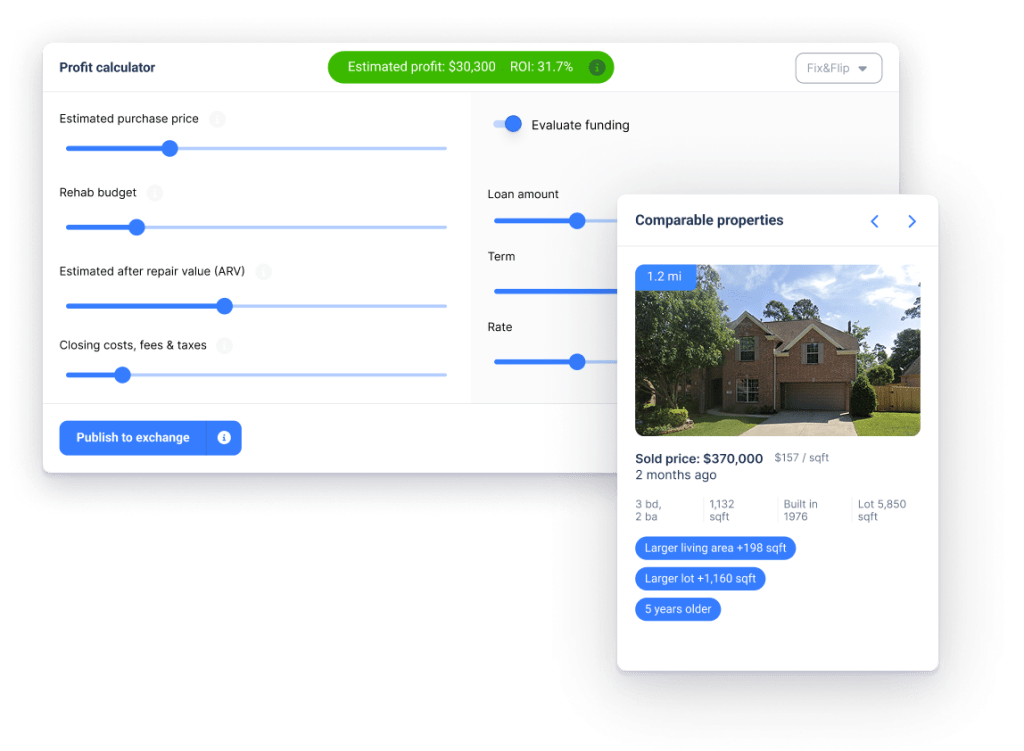

After Repair Value (ARV) This is the estimated value of the property after all renovations are complete. Most lenders will loan 70 to 80% of the ARV. So if a property will be worth $300,000 after repairs, a lender might offer up to $210,000 to $240,000.

You can learn more about how ARV is calculated on Investopedia.

Loan-to-Cost (LTC) Some lenders base their loan on the total cost of the project (purchase price plus renovation budget) rather than ARV. Typical LTC ratios are 80 to 90%.

Your project plan Even as a beginner with no track record, a clear and detailed project plan goes a long way. Lenders want to see that you understand the scope of renovations, have realistic cost estimates, and have a clear exit strategy (sell the property by a specific date).

Experience This is where beginners often worry most. The good news is that many hard money lenders specifically work with first-time flippers. Having no track record is not a dealbreaker as long as your deal makes sense on paper. If you can show a solid ARV, a realistic renovation budget, and comparable sales in the area, most lenders will take you seriously.

Credit score Hard money lenders care less about your credit score than a bank would, but most still have a minimum threshold, typically around 600 to 650. Some will go lower if the deal is strong enough.

Step 2: Run the Numbers Before You Apply

The single biggest mistake beginners make when applying for fix and flip loans for beginners is approaching a lender before they understand their own deal. Lenders can tell immediately whether you have done your homework, and showing up unprepared kills deals fast.

Before you contact any lender, you should know:

- The purchase price of the property

- Your estimated renovation costs (broken down by category if possible)

- The ARV based on comparable sales in the area

- Your expected profit margin after loan costs, renovation, and selling expenses

- Your timeline from purchase to sale

LendingExchange has a free Real Estate Calculator that walks you through all of these numbers. You can estimate costs, calculate ARV, and see your projected return before you ever talk to a lender. Using a tool like this also shows lenders that you are serious and organized, which matters more than you might think for a first-time borrower.

A basic formula to check before applying:

ARV x 0.70 = Maximum all-in cost (purchase plus renovation)

If your purchase price plus renovation budget is under that number, you are in a good position. If it is over, you need to renegotiate the purchase price or reconsider the deal.

Step 3: Build Your Project Package

Building a strong project package is one of the most overlooked steps when pursuing fix and flip loans for beginners. Think of your project package as your loan application before the loan application. It is a simple document that organizes everything a lender needs to evaluate your deal quickly.

A solid beginner project package includes:

- Property address and photos of current condition

- Purchase price and how you arrived at it

- Renovation scope with line-item cost estimates

- Three to five comparable sales (comps) in the area from the last 6 months

- Your ARV estimate based on those comps

- A timeline from closing to renovation completion to sale

- Your exit strategy (sell outright, refinance, etc.)

You do not need to be a professional to put this together. County records, Zillow, and Redfin give you comp data. Local contractors can provide renovation estimates. The more organized your package is, the faster lenders can say yes.

Step 4: Finding the Right Lender for Fix and Flip Loans for Beginners

Not all hard money lenders work with beginners. Some require a minimum number of completed flips before they will fund a deal. Finding lenders who specifically welcome first-time investors saves you a lot of wasted time and rejection.

When evaluating lenders, look for:

- Experience working with first-time flippers (ask directly)

- Transparent fee structures with no hidden costs

- Reasonable closing timelines (7 to 21 days is standard)

- Clear communication and responsiveness

- Willingness to explain terms without pressure

LendingExchange lets you post your project and receive offers from vetted lenders who are open to working with beginners. You can compare rates, fees, and terms side by side, and communicate directly with lenders through the platform before committing to anything.

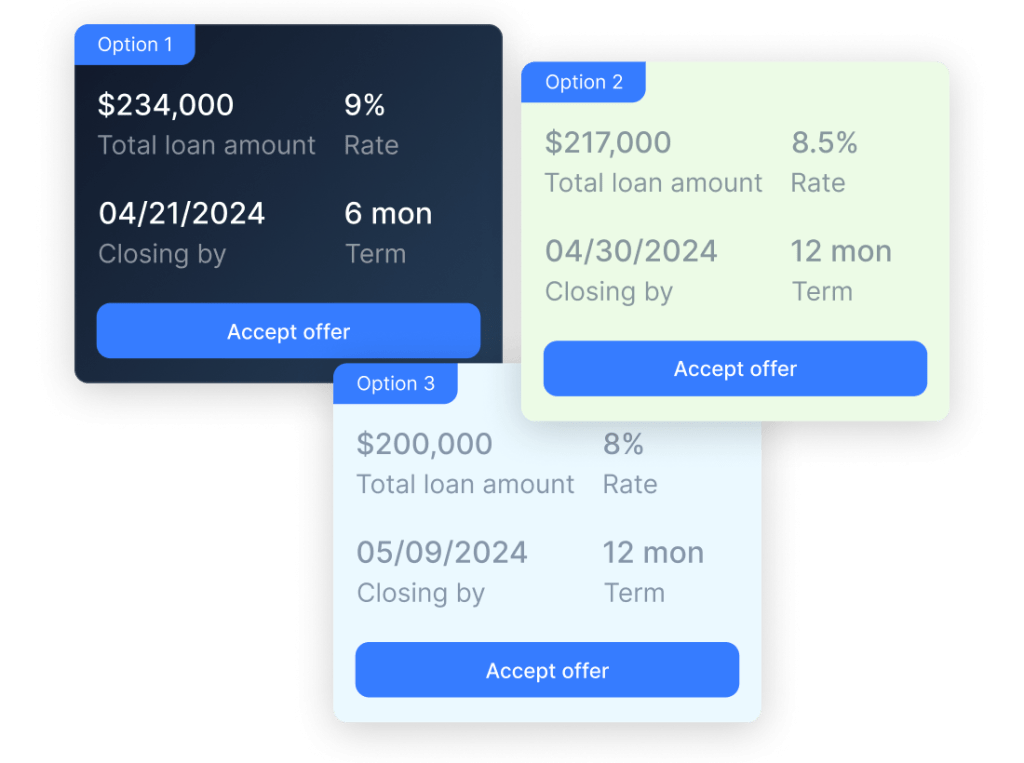

Step 5: Compare Loan Offers the Right Way

Comparing offers is where many fix and flip loans for beginners go wrong — most people focus only on the interest rate and miss the bigger picture.When offers come in, do not just look at the interest rate. The total cost of the loan matters more than any single number.

Here is what to compare across offers:

Interest rate Typically quoted as an annual rate. Hard money rates range from 8 to 15% for most deals. A 1% difference on a 6-month loan is meaningful but not the only factor.

Points (origination fees) Most hard money lenders charge 1 to 3 points upfront. One point equals 1% of the loan amount. On a $200,000 loan, 2 points means $4,000 due at closing.

Loan term Make sure the term gives you enough time to complete renovations and sell. If you think the project takes 6 months, a 9-month term gives you buffer. Running out of time on a hard money loan is expensive.

Extension options Ask whether you can extend the loan if the project runs long, and what that costs. Most lenders offer extensions but charge additional fees.

Draw schedule for renovation funds Some lenders release renovation funds in draws as work is completed rather than all at once. Understand how this works before you sign.

Prepayment penalties If you sell faster than expected, will you be penalized for paying the loan off early? Many hard money lenders do not charge prepayment penalties but some do.

Step 6: Common Mistakes to Avoid with Fix and Flip Loans for Beginners

Learning from others is faster and cheaper than learning from your own errors. Here are the most common mistakes beginners make with fix and flip loans:

Underestimating renovation costs This is the number one deal killer. Get real contractor bids, not rough estimates, before you commit to a purchase price. Add a 10 to 15% buffer on top of your best estimate for unexpected issues.

Overestimating ARV Be conservative with your after-repair value. Use comps that are truly comparable in size, condition, and location. Do not cherry-pick the highest sale in the area.

Ignoring holding costs Every month you own the property costs money. Loan interest, property taxes, insurance, and utilities add up fast. A deal that looks great on paper can lose money if the renovation takes twice as long as planned.

Not having a backup plan What happens if the property does not sell as fast as you expect? Have a plan B, whether that is renting the property temporarily, reducing the price, or refinancing into a longer-term loan.

Taking the first offer Always compare at least two to three lenders before committing. Fees and terms vary significantly and a few hours of comparison can save you thousands.

Fix and Flip Loan Glossary for Beginners

Before diving into fix and flip loans for beginners, it helps to know the key terms lenders use when evaluating your deal.

ARV (After Repair Value): The estimated market value of a property after all planned renovations are complete.

Hard money loan: A short-term loan from a private lender, secured by the property, typically used for fix and flip projects.

LTV (Loan-to-Value): The loan amount as a percentage of the property value. An 80% LTV on a $200,000 ARV means an $160,000 loan.

LTC (Loan-to-Cost): The loan amount as a percentage of the total project cost (purchase plus renovation).

Points: Upfront fees charged by lenders, expressed as a percentage of the loan amount. One point equals 1%.

Draw: A disbursement of renovation funds released by the lender in stages as work is completed.

Bridge loan: A short-term loan that bridges the gap between buying a property and selling or refinancing it.

Exit strategy: Your plan for paying off the loan, typically selling the property or refinancing into a longer-term product.

Start Your First Fix and Flip Deal

Fix and flip loans for beginners are more accessible than most people realize. Lenders who work with new investors exist, the tools to run your numbers are free, and a solid deal with a clear plan will get funded even without a track record.

The key is showing up prepared. Know your numbers, have a project plan, and compare your options before committing.

Use the free Real Estate Calculator at LendingExchange.io to estimate your deal, then post your project to connect with lenders who work with beginners. No pressure, no unwanted calls — just the information you need to make a confident first move.